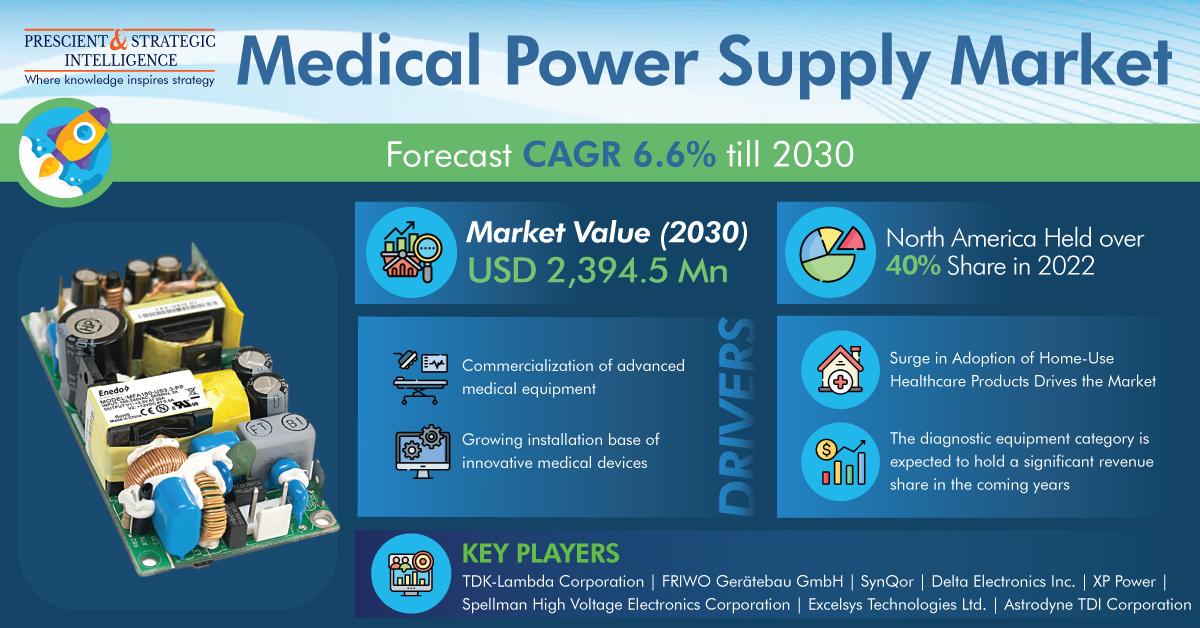

The total revenue of the medical power supply market was USD 1,432.2 million in 2022, which will reach USD 2,394.5 million by 2030, powering at a rate of 6.6% in the years to come, as per a report by P&S Intelligence.

The use of home-use healthcare devices is on the rise, because of the aging populace's increased tendency for developing chronic diseases. Therefore, an extraordinary boost in house-based healthcare will yield profitable prospects for market players, leading to the expansion of compact and effective supply units.

Moreover, the increased use of moveable and integrated medical gadgets, an increase in the tendency of consumers for the use of healthcare items for home, and an increase in requirement for lightweight, house-based equipment will power the industry.

Also, the market will rise because of increased consciousness of the benefits of medicinal power supplies, as well as restored thermal management, better power factor correction, and less perceptible noise.

The medical power supply market is characterized into open frame, enclosed external, U bracket, configurable, and encapsulated. The enclosed category will dominate in the industry, with about 40%, in 2022.

This is because of the quick obtainability of cutting-edge, small, enclosed sources of power having high competence and low leakage current, resulting in less power use.

The diagnostic equipment category will have a significant share of revenue. In the domains of diagnostics, monitoring technologies, medical imaging, and therapeutics, power supply goods and technology has an important role.

Therefore, supply of voltage power and X-ray generator solutions allow and improve the provision of treatment, from making X-rays to powering detectors.

Furthermore, the requirement for monitoring and diagnostic equipment is expanding because of more government efforts for diagnosing infectious diseases and the increasing need for fast detection of disease.

Likewise, companies are aggressively funding many research projects, for example those for the early discovering of communicable diseases.

North America dominated the industry, with over 40% share, in the past. This is for the reason that, the clinical industry is in the phase of transition from a volume-based to a value-based model.

Furthermore, superior clinical care, better scan detection, shorter stays at the hospital, and the evading of developing ailments are powering the requirement for advanced medical equipment.

Europe followed North America, with around 30% share in the past. A few main factors fast-tracking the growth rate of the European industry are the surge in the occurrence of diseases, improved access to patient care, the obtainability of tech support for healthcare, the increase in the standard of living, and the efficiency of digitally controlled power supply.

Due to the commercialization of the advancement of the medical equipment, the demand for medical power supply will increase considerably in the future.

SOURCE: P&S Intelligence